Year-End 2019 Sentiment Survey Results: Survey Says—Another Up Year in 2020

Headlines from this article:

- The RCLCO Current Real Estate Market Sentiment Index (RMI) has increased 27.4 points over the past year, from 37.5 at YE 2018 to 64.9 at YE 2019, slightly below the Mid-2018 RMI (68.4).

- Respondents predict that real estate market conditions will worsen slightly in the near future, with the RMI anticipated to drop approximately 13 points to 52.3 over the next 12 months.

- Approximately 8 out of 10 survey respondents (77%) believe the downturn will not occur until 2021 at the earliest, with 37% not predicting the downturn until 2022 or later. The next downturn is considered to be much less imminent than it was a year ago (YE 2018), when 46% of respondents believed the downturn would begin in 2019 or had already begun.

- Most respondents (64%) indicated that they would not rent office space to WeWork if they were an office landlord. Conversely, 71% indicated that they would rent office space to a different coworking company.

- Consistent with the findings of the Mid-2019 survey, respondents indicate that most product types remain firmly in the “late stable” phase of the real estate cycle, with all uses except retail easing back from the cycle peak relative to YE 2018 sentiments. The product types not yet in the “late stable” phase are on the cusp between “early stable” and “late stable.”

- Respondents anticipate that within the next 12 months, retail will have moved past the peak and into the “early downturn” phase, with several other product types on the verge.

Over the past few years, RCLCO Sentiment Surveys had indicated continued confidence in real estate market conditions. This trend was bucked at the end of 2018 when, amidst rising concerns surrounding the state of the economy and the stock market, respondents to the YE 2018 Sentiment Survey reported deteriorating market conditions and warned of a forthcoming recession.

In the two surveys since YE 2018, respondents have become far more optimistic, as radically improving stock market conditions and resilient underlying real estate fundamentals have given reason for optimism. Although respondents to the YE 2019 Sentiment Survey believe that most real estate sectors are firmly in the “late stable” stage of the cycle, the general sentiment is that most asset types are not quite as close to the “early downturn” phase as they had predicted a year ago. While market sentiment levels are slightly lower than they were in the Mid-2018 survey, the return to similar levels of optimism is cause for confidence in the near term.

Overall Sentiment Has Consistently Improved in Recent Surveys, after YE 2018 Results Suggested a Cratering in Overall Sentiment

While the sentiment surrounding the current national real estate market is noticeably more optimistic than it was in YE 2018 (one year ago), and slightly more optimistic than it was in Mid-2019 (six months ago), sentiments are now approaching the levels of the Mid-2018 survey. Just over one-tenth (13%) of respondents to the most recent survey say national real estate market conditions are moderately or significantly worse today than they were a year ago. This is 16 percentage points lower than in the Mid-2019 survey, 35 percentage points lower than the YE 2018 survey, and on par with results of the Mid-2018 survey (15%). Conversely, the share of respondents reporting better market conditions today than one year ago increased to 43%. This is 16 percentage points higher than the Mid-2019 survey (27%), 20 percentage points higher than the YE 2018 survey (23%), and nine percentage points lower than in Mid-2018 (52%). This indicates that while sentiments are far more optimistic than they were a year ago, sentiment is generally similar to Mid-2018.

How Would You Rate National Real Estate Market Conditions Today Compared With One Year Ago?

Current U.S. Market Sentiment over Time

Source: RCLCO

The cratering of market sentiment at the close of 2018, and the ensuing yearlong rebound, has been reflected in RCLCO’s Real Estate Market Index (RMI),[1] which measures sentiment on a 100-point scale. Responses from the YE 2019 survey generate a current RMI of 64.9, which constitutes a 27.4-point yearlong climb from the low point in YE 2018 (37.5). It should be noted, however, that the Mid-2018 RMI registered at 68.4, suggesting that while the improvement in market sentiment between YE 2018 and YE 2019 indicates optimism about current market conditions, it is more of a return to the trend in the years leading up to Mid-2018 than it is a sign of unprecedentedly strong market conditions.

In addition to reflecting upon the past year, respondents were asked to predict how the U.S. economy and real estate markets would perform over the upcoming year. Since Mid-2015, respondents have predicted that the U.S. economy and real estate markets would be in worse shape a year from the survey than they were at the time the survey was taken. This tendency is reflected in the predicted RMI, which is consistently registering between 8 and 14 points lower than the current RMI. The results of the YE 2019 survey are no different, producing a predicted RMI of 52.3, approximately 13 points lower than the current RMI (64.9).

Despite the consistency of this phenomenon, RCLCO believes that the reasons underlying the lower predicted RMI vary from survey to survey. For example, despite a strong RMI of 68.4 in the Mid-2018 survey, the predicted RMI was approximately 14 points lower. This result suggested that conditions were so strong at the time, and the recovery had already lasted so long, that respondents believed it was not likely that conditions would be as strong in the future. Contrast this with the YE 2018 survey, where the predicted RMI (26.2) was approximately 11 points lower than the current RMI (37.5). Despite a similar decrease in predicted RMI, the underlying takeaway from this survey was completely different than Mid-2018, as many respondents believed that conditions had gotten so poor that a downturn was coming within the next year. In the case of the most recent survey, RCLCO believes that respondents are more aligned with those of Mid-2018, with the decrease in predicted RMI more of a belief that current healthy market conditions are too good to last at this level for the next year.

RCLCO National Real Estate Market Index

Source: RCLCO

Between the YE 2011 and Mid-2018 surveys, the proportion of respondents predicting improving conditions over the upcoming year consistently outweighed the proportions predicting worsening or unchanged conditions, a signal of the consistent forward-looking optimism exuded by respondents during this period. The dramatic swing toward pessimism at the end of 2018 was captured in the YE 2018 results, as approximately 60% of respondents predicted worsening conditions over the next 12 months. The pessimism has subsided over the past two surveys, and, for the first time since the Mid-2018 survey, more respondents predicted improving conditions (31%) than worsening conditions (27%). It should be noted that the plurality of respondents believe conditions will remain largely unchanged (42%), the highest percentage since Mid-2011, which helps keep in context that the optimism of the most recent survey results is slightly muted.

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Respondents Indicate That the Downturn Is Unlikely to Occur within the Next 12 Months

Prior to the YE 2018 survey, respondents had on average demonstrated a tendency to push off the anticipated timing of the next downturn approximately two years from the date of the survey. In the YE 2018 survey, however, respondents curbed this tendency, with 45% of respondents predicting that the downturn would be upon us by the end of 2019, including 20% of respondents who suggested that the downturn had already begun.

As was the case in Mid-2019, results from the YE 2019 survey suggest that respondents have fully returned to their tendency to “push off” the predicted timing of the next downturn until several years down the road. Approximately 77% of YE 2019 respondents predict that the recession will not occur until 2021, at the earliest, including 37% of respondents who believe that the downtown will not occur until at least 2022. The proportion of respondents who believe that the downturn is already upon us, or will occur sometime within the next year, comprise a relatively small proportion (24%) of respondents, another sign of moderate optimism among survey respondents.

Real Estate Downturn Timing Predictions over Time

Source: RCLCO

The Majority of Respondents Would Not Rent Office Space to WeWork, But Would Rent to Another Co-Working Company

In addition to the broader questions regarding the overall health and near-term outlook for the national real estate markets, RCLCO typically asks respondents to weigh in on a specific topic of current interest. Respondents to the YE 2019 survey were asked the following questions:

- If you owned an office building, would you rent part of it to WeWork?

- Would you rent part of it to another coworking company?

Almost two-thirds (64%) of respondents would not choose to rent any of their space to WeWork. Among these respondents who would not rent to WeWork, approximately 58% (37% of all respondents) would consider renting to a different coworking company.

Conversely, 36% of respondents would rent a portion of their space to WeWork. Out of this pool, approximately 95% would also rent space to a different coworking company.

Source: RCLCO

Overall, 71% of respondents indicated that they would rent to a different coworking company than WeWork, compared with just 36% that would rent to WeWork. Respondents were given an opportunity to provide their rationale for their responses; the following responses were most common:

Would rent to WeWork and would rent to another company

- Coworking can be a stable source of income, as long as it is not the lead tenant

- WeWork and other coworking companies add diversity to an office building

Would rent to WeWork but would not to another company

- Trust/guarantees in the brand name WeWork that smaller companies do not offer

Would not Rent to WeWork but would rent to another company

- The financial instability of WeWork is too risky

- Coworking as a concept is a viable business model

Would not rent to WeWork or to another coworking company

- Coworking is an unstable business model that puts the landlord at risk

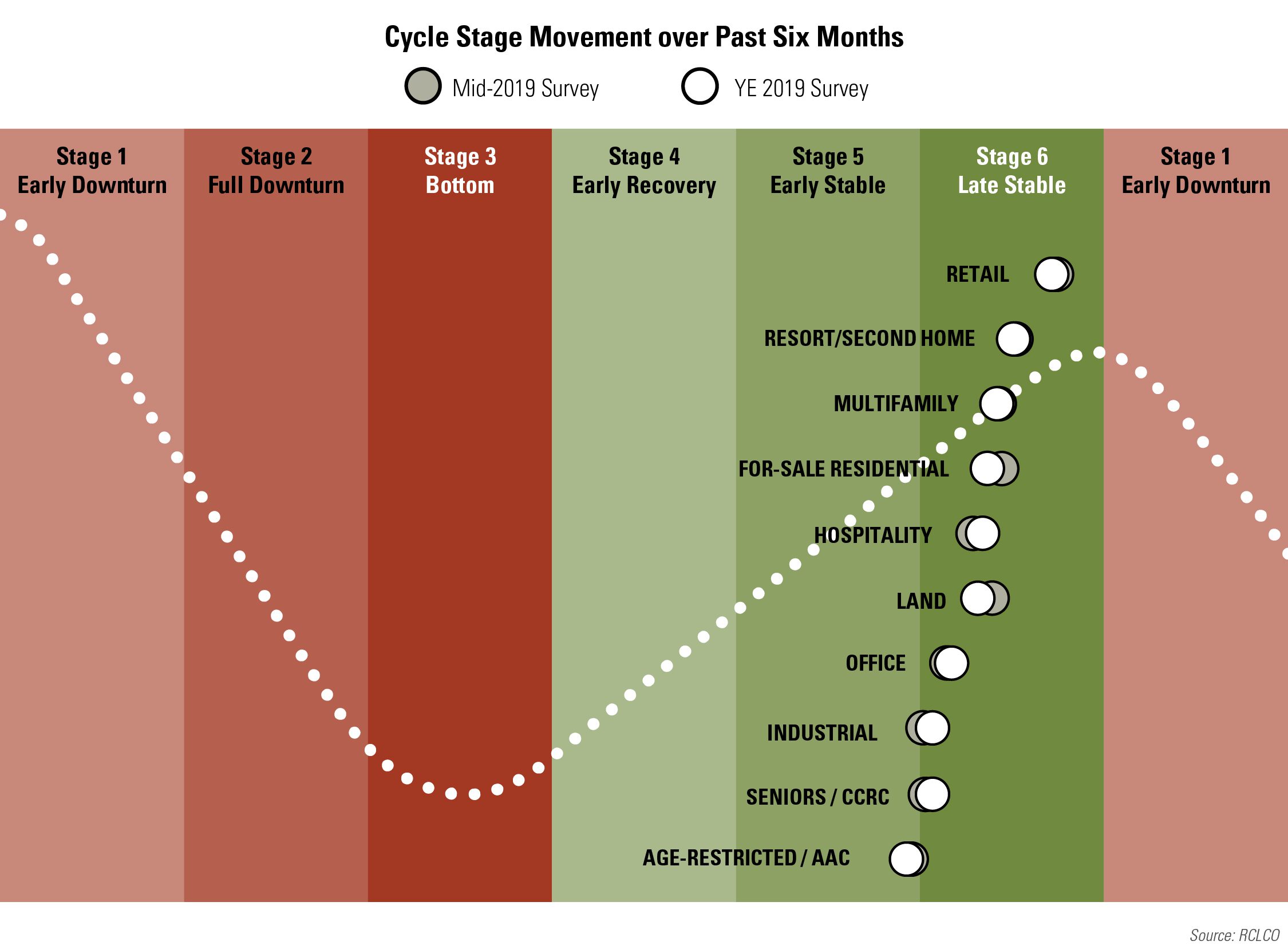

Not Much Change in Cycle Locations for a Majority of Product Types over the Past Six Months

Respondents to the YE 2018 survey reported notable cycle movement for most product types over the previous six months, positioning all products either firmly in or creeping towards the “late stable” phase of the real estate cycle. Six months later, respondents to the Mid-2019 survey significantly modified the locations of all product types, except retail, back away from the peak. YE 2019 positions for retail, for-sale residential, land, hospitality, office, and age-restricted/AAC are significantly closer to the peak than they were in Mid-2018. However, these sectors remain largely unchanged, or even further from the peak, than in Mid-2019. The multifamily, industrial, and seniors/CCRC positions have not changed much at all since Mid-2018.

As was the case in Mid-2019, YE 2019 respondents placed retail, resort/second home, for-sale residential, multifamily, land, hospitality, and office definitively in the “late stable” phase, with age-restricted/AAC, seniors/CCRC, and industrial uses remaining on the edge between “early stable” and “late stable.” Although the various product types are positioned differently within the “late stable” phase, their current positions and recent movement away from the “early downturn” stage are consistent with the general sentiment that the downturn is approaching, but not imminent.

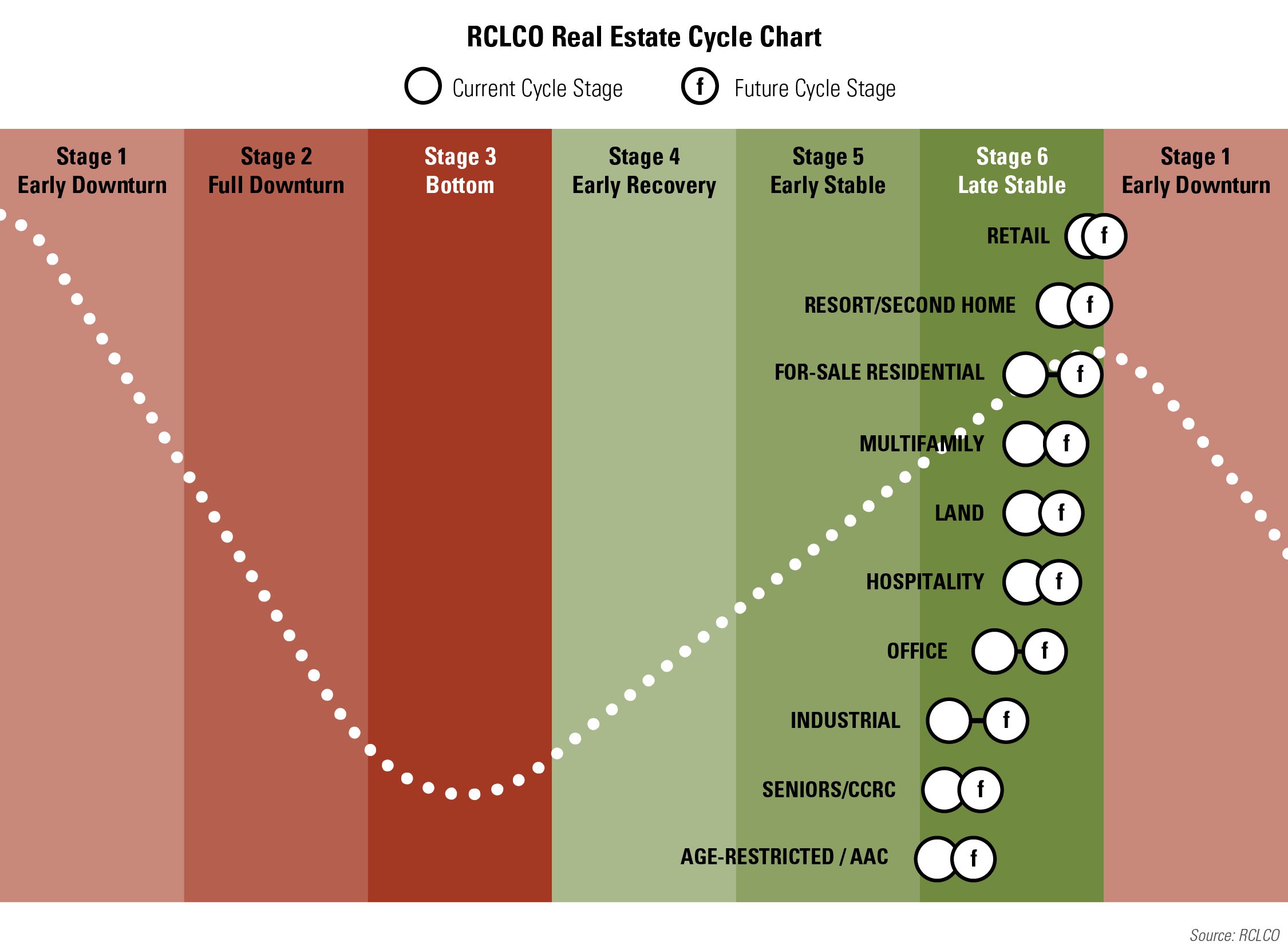

Retail Anticipated to Cross the Threshold into “Early Downturn” Phase, but Resort/Second Home Is No Longer Expected to Join

Much as in the Mid-2019 survey, YE 2019 survey respondents believe that all land uses will be at least in the “late stable” phase within the next 12 months, with retail predicted to be the only land use crossing into the “early downturn” phase. In Mid-2019, respondents thought that Resort/Second Home would also be in “early downturn” within the next 12 months; however, YE 2019 respondents have tempered this prediction, placing resort/second home at the end of the “late stable” phase, along with for-sale residential. Multifamily, land, hospitality, and office are expected to move closer to the end of the “late stable” stage, while industrial, seniors/CCRC, and age-restricted/AAC are all expected to move closer to the early/middle portions of the “late stable” phase.

Share of Respondents Believing Current Downturn Conditions and Predicting Downturn in Next 12 Months Increases Among All Land Uses

While the majority of respondents do not believe that any product types are currently in downturn, the proportion of respondents who do believe product types are already in downturn has dramatically increased since the Mid-2018 survey for almost all land uses (with the exception of multifamily). The most dramatic examples of this are resort/second home, with 38% of respondents indicating current downturn conditions (up 18 percentage points since Mid-2018), and seniors/CCRC, currently around 17% (up 11 percentage points). Other notable, but slightly less dramatic, changes involve land, for-sale residential, hospitality, and retail. All of these sectors have seen the proportions indicating current downturn conditions increase by about 9% since Mid-2018. Despite these significant increases since Mid-2018, YE 2019 respondents are still noticeably less pessimistic about the location of most product types in the cycle than respondents were in YE 2018.

Share of Respondents Believing Current Downturn Conditions

Source: RCLCO

Respondents believe that all product types are more likely to be in downturn in 12 months than they are now. By 12 months from now, the majority of respondents expect a few land uses to be in downturn. The YE 2019 survey indicates that 61% of respondents expect retail to be in downturn (up approximately 10 percentage points from the 52% of respondents who believe it is currently in downturn), along with 55% for resort/second home (up 17 percentage points). The asset type with the next largest proportion of respondents anticipating a downturn is office, which 40% of respondents predict will be in downturn within 12 months (up 18 percentage points).

Share of Respondents Believing Current Downturn Conditions and Predicting Downturn Conditions over the Next 12 Months

Source: RCLCO

RCLCO’s Point of View for Real Estate: Current and Near-Term Outlook (As of January 2020)

The outlook for the U.S. economy is that 2020 should be a relatively good year. The storm clouds that had been gathering in 2018 and 2019, driven in large measure by an (albeit briefly) inverted yield curve, an escalating trade war with China (and a bunch of other countries), and the threat of war in the Middle East (ok, this was actually in the first week of 2020), seem to have dissipated. The consensus forecast is that U.S. economic growth will be 2.0%, and that recession risks will be contained in 2020.

Steady economic growth and positive consumer sentiment should be good for real estate in the near term. Residential building permits increased in the latter half of 2019 to a seasonally adjusted annual rate of 1.4 million units, aided by continued low interest rates, and existing home prices have risen at nearly 6% per year[2] since hitting the bottom nearly a decade ago. Commercial real estate values have increased even more than home prices since the Great Recession, increasing approximately 8%[3] per year. Prices are up across all product types, but apartments and industrial continue to be the leading real estate sectors. Cap rates remain at historically low levels, falling into the low to middle single-digit range across all product types. Increased allocations by institutional investors to real estate and significant “dry powder” growth globally suggest that investors believe real estate will outperform other asset classes.

While the economic outlook for 2020 looks positive, the downside risks to continued growth and increasing real estate valuations are considerable. There remain significant geopolitical uncertainties, ranging from potential continued global trade issues, to Brexit, to a U.S. presidential election that could have an impact on everything from trade to immigration, taxes, and foreign policy—all of which pose serious threats to continued expansion and consumer confidence. Commercial real estate values are particularly vulnerable to increases in interest rates. Home price appreciation is forecasted to moderate to a more normal rate of 3% per annum consistent with household income growth, and commercial real estate values are expected to remain essentially flat over the next 12 to 24 months. Some property types and markets are already experiencing downturn conditions: retail continues to suffer from changing consumer preferences, e-commerce impacts, and oversupply; Houston continues to emerge from the impacts of the 2015 correction in energy prices; and most reading this can, no doubt, identify sources of heartburn in their own segments, markets, or submarkets.

This relatively optimistic outlook for 2020 is, of course, predicated upon the assumption that the U.S. economy, real estate sector, and stock market continue to operate without any significant disruption. As the old saw goes, real estate expansions do not die of old age—and this one is now officially the longest expansion in U.S. post-war history at 127+ months. No, economic downturns are precipitated by pressure or “shocks” to the system that hurt demand for real estate and/or disrupt the normal flow of capital and credit and expose asset pricing bubbles. The good news is that there don’t appear to be any obvious asset bubbles in the real estate sector. Many believe that the stock market is overvalued, and while this may be true by historical standards, it is important to remember that the stock market is not the economy. Corporate debt, and the erosion of underwriting standards in the corporate loan and bond markets—particularly driven by aggressive lending by nonbanks—are a growing concern. And perhaps of most concern is the fact that the Fed may have little “dry powder” to provide fiscal stimulus to contain the potential bursting of any asset bubble. And, of course, there is the fact that historically, an inverted yield curve has always preceded an economic downturn by 12 to 24 months, placing 2020 in the bullseye for such event. Who knows…?

With this in mind, the RCLCO Sentiment Survey respondents are probably not wrong that the likelihood of a downturn in 2020 is small. However, the 37% of survey respondents who predict the next downturn will arrive in 2022 or later may be overly optimistic. The risk that the U.S. economy, and therefore the real estate markets, will experience a period of slower growth (a.k.a. a recession) sometime over the next two years increases with each month that is added to the expansion record books. Not because of any “known knowns,” to cite a famous former defense secretary, but because history does have a tendency to (eventually) repeat itself.

And even if the next downturn doesn’t come until 2022 or beyond, a delayed recession should not lead to complacency—there are plenty of other challenges that the lengthy expansion has to offer. Changing demographics and consumer preferences are already creating winners and losers by property type and geography. Labor shortages drive delays and cost overruns, and even temporary liquidity “hiccups” can challenge risky capital structures. Real estate owners, investors, and developers would be wise to be careful—tighten up underwriting standards; maintain a conservative leverage at the asset, portfolio, and enterprise levels; and focus on delivering sound operating fundamentals in the event that the markets deliver a surprise—and remember, it is almost always a surprise!

Thoughts to Ponder

There are some long-term and broader issues to consider when formulating a point of view about the longer-term future:

- Demographics—How will the aging population of America, coupled with restrictive immigration policies, impact the U.S. economy in the long run? What are the pitfalls and the opportunities they create?

- Economic growth—Is the current growth cycle fueled by fundamentals of supply and demand for goods and services, or is it fueled by easy money policies? In other words, is growth real or is it an illusion?

- Can economic growth persist without dire side-effects of global warming and rising inequality across the globe? Are there silver linings and/or business opportunities in these mega trends?

- What are the consequences of digitization and reinvention of how we live, shop, learn, and work?

These and other weighty macro issues are worthy of discussion as executive teams and corporate boards consider enterprise strategies.

Strategies for the Cycle

Strategies that real estate companies and investors should be considering at this point in the cycle include:

- Debt—Manage debt levels and maturities now, if you have not already done so, to maintain liquidity and avoid significant recaps in the 2021-2022 timeframe

- Underwriting—Tighten underwriting standards and get real about both revenue growth and cost escalations in your pro formas

- Sell—Evaluate the exit of any marginal assets, deals, markets, businesses; now may be the best time for anything you plan to divest yourself of over the next 12-24 months

- Partner/Outsource—Resist the temptation to self-perform peak activity, and lay off some of the excess work to others, so as to avoid painful RIFs in a possible downturn

- Capital—Identify/line up equity capital now for opportunistic investments that will likely be present in the next downturn and invest/execute when others can’t/won’t

Who Took the Survey?

RCLCO’s Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and across the industry. Approximately two-thirds (65%) of respondents have worked in the real estate industry for 20 years or more, and 79% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 39% of the sample. Another 17% are investors or capital allocators, followed by 10% in design or architecture firms. The remaining 34% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole; however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

Sentiment Survey article and research prepared by Leonard Bogorad, Managing Director, and Maury Winter, Associate. RCLCO Point of View prepared by Charles Hewlett, Managing Director.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

[2] CoreLogic National House Price Index

[3] Moody’s Analytics Commercial Property Price Index

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us