Records Are Falling, but Don’t Drop Your Guard Just Yet…

Real Estate Cycle Planning for Your Company Is as Important as Ever.

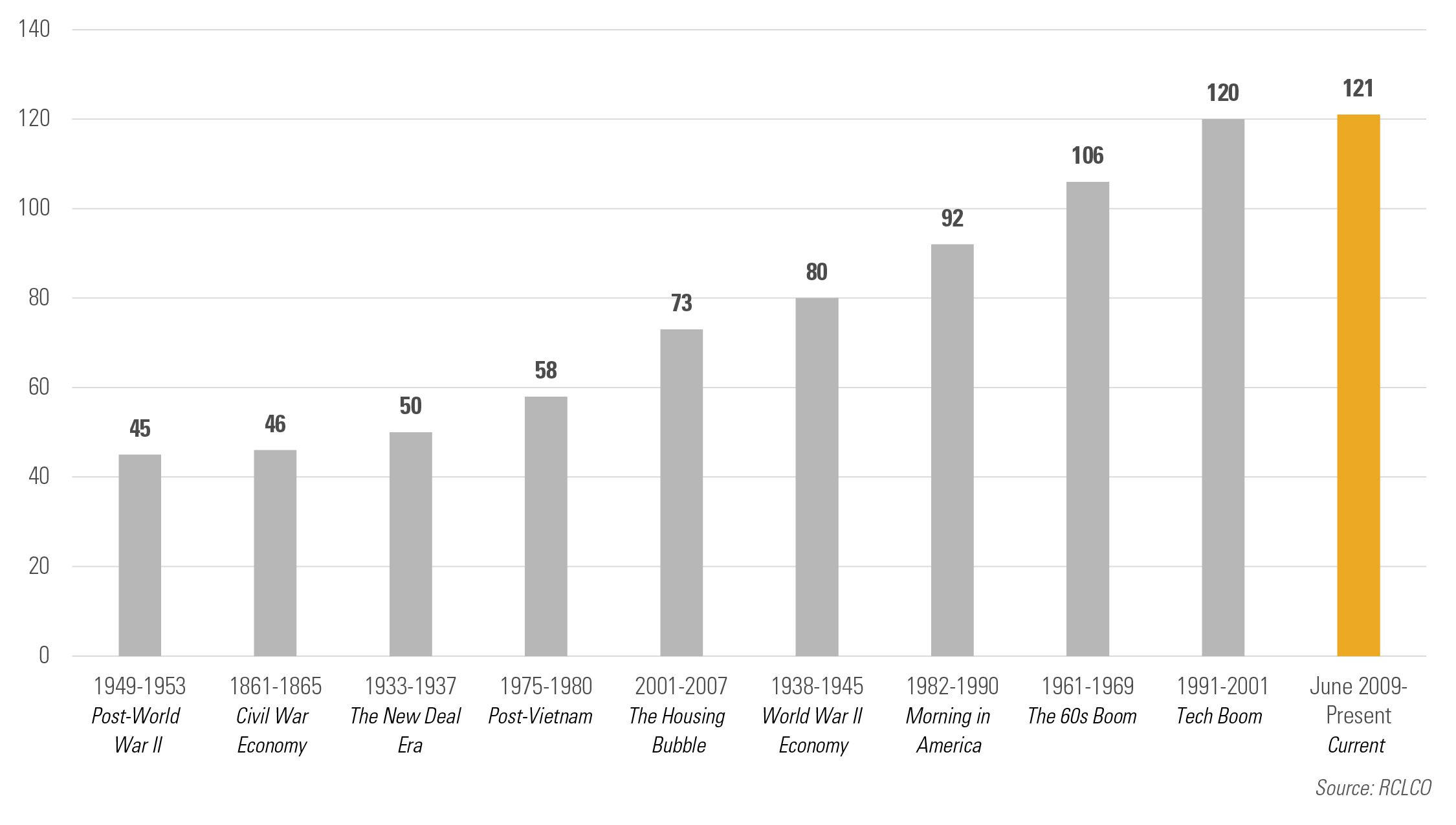

The U.S. broke its record for time without an economic recession Monday as it began the 121st consecutive month of gross domestic product (GDP) growth since the 2008 recession. The recovery, which began in July 2009, turned 10 years old Monday, marking the longest stretch of economic expansion in modern U.S. history.

Longest Economic Expansions in U.S. History

(Number of Months)

As indicated in the most recent RCLCO Sentiment Survey, real estate market participants have pulled back somewhat on recent pessimism, as improving stock market conditions and resilient underlying real estate fundamentals have given reason for moderate optimism. But that does not mean that we should defer planning for the next downturn.

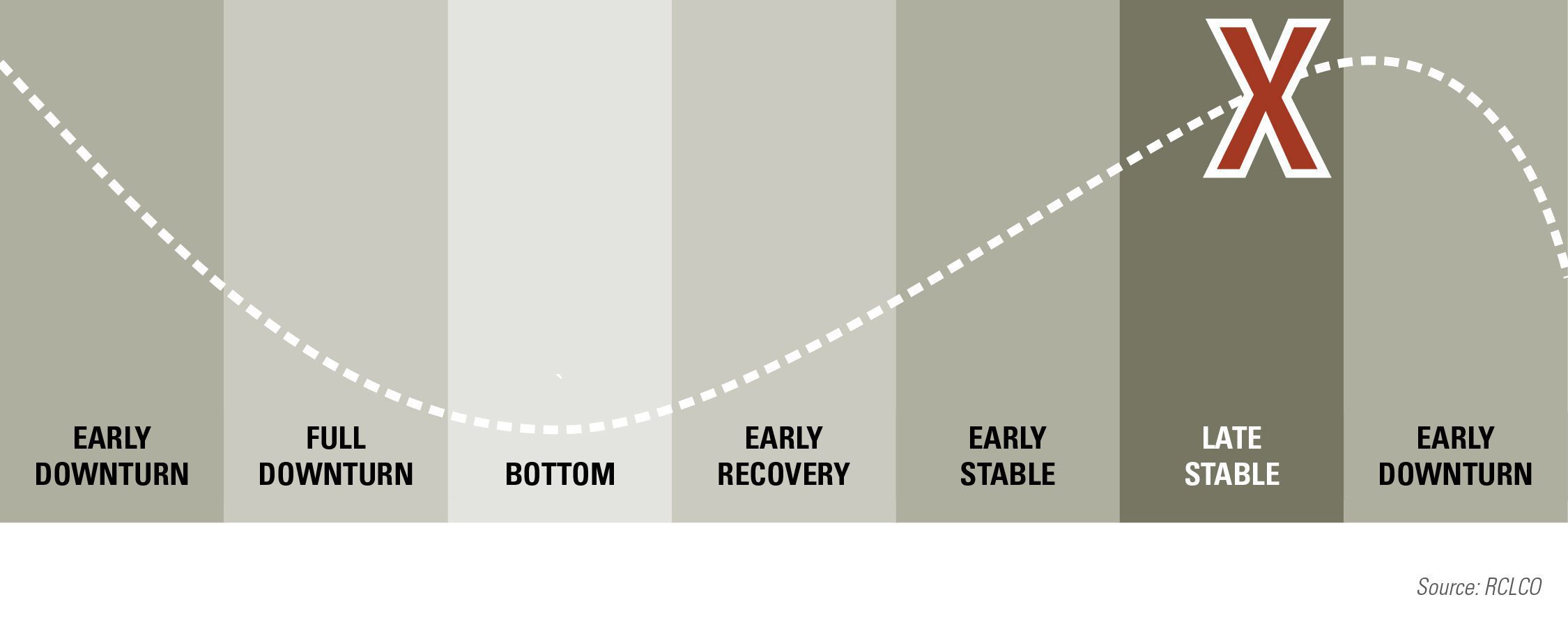

Real estate has continued to benefit from an expanding U.S. economy, with fundamentals either continuing to improve or holding steady across all asset types. Pricing and transaction volume continue to be buoyed by yield-seeking capital, as interest rates have declined over the past quarter. While operating fundamentals remain strong, growth rates have tempered, which, combined with capital market risks, indicates that real estate may be nearing the end of the “late stable” stage of the market cycle, and heading into an “early downturn.” This is consistent with the opinions of Sentiment Survey respondents.

After flirting with inversion during the early part of the year, the yield curve has maintained an inverted form over recent weeks, hinting that there is risk of recession within the near- to medium-term. When it occurs, real estate will experience some pain, even if not to the same degree as during the last downturn. Absorption may no longer keep up with deliveries of new multifamily and industrial buildings, and office and retail assets may struggle to maintain occupancy in the face of changing demand characteristics.

There is still more capital than there are good real estate opportunities that meet return expectations, and capital stacks at the asset level have been constructed more conservatively in the upturn phase of this cycle, so we don’t expect to see that much stress in the system. And while we don’t expect to see a repeat of the dislocation experienced during the Great Recession, there will still be opportunities in the next downturn. Accordingly, we recommend that market participants keep some “dry powder” available for opportunistic buys. Equal attention should be paid in the latter stages of the expansion to “eyes wide open” underwriting, and income and value creation through focused operations. Real estate investors should underwrite with realistic assumptions about future income and expense escalations, and test for downside protection and make sure they are comfortable with the results.

Property Markets Outlook

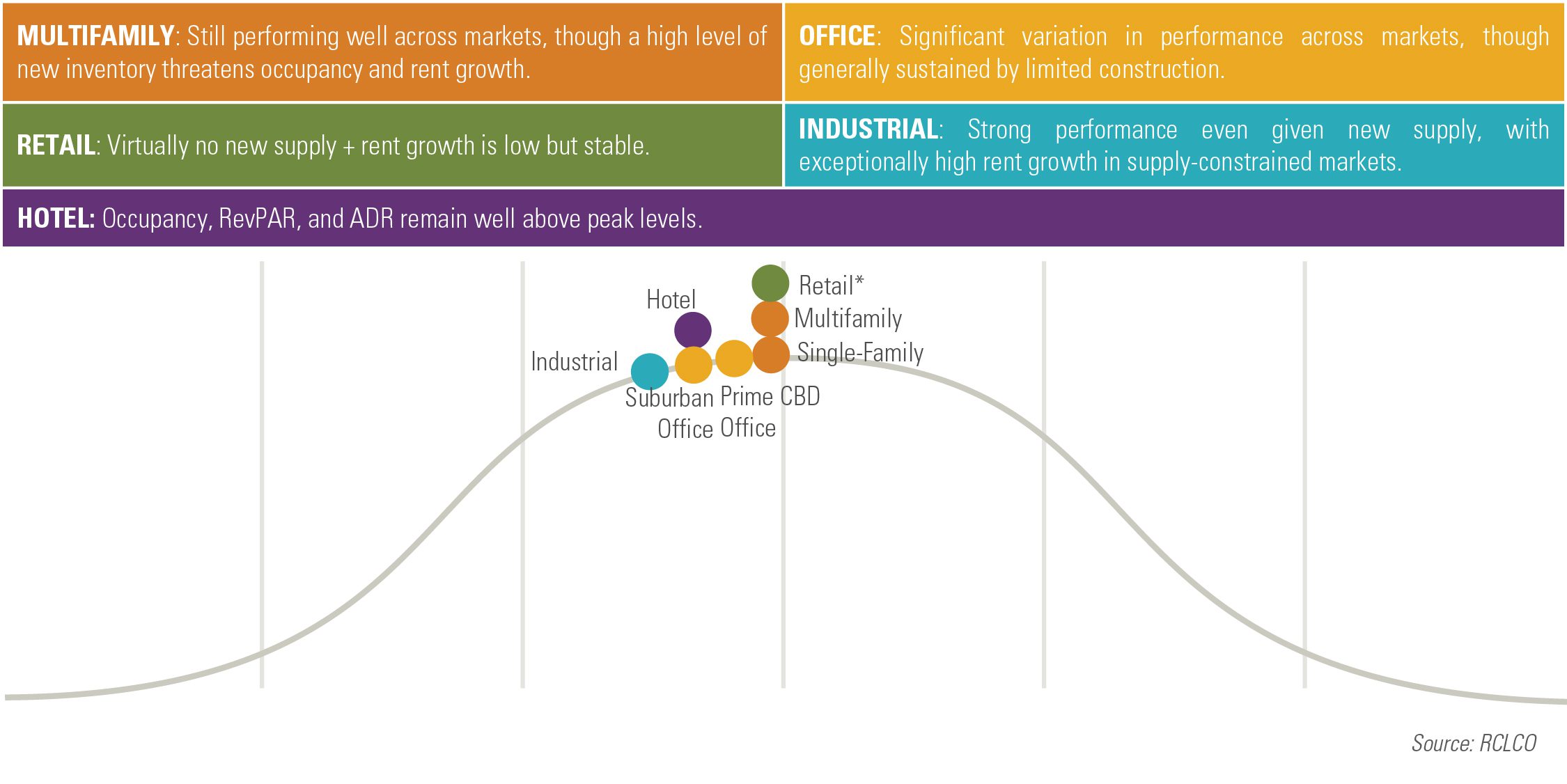

Two general stories have emerged in real estate property markets in recent years. The first, which can be applied to multifamily and industrial real estate, is one of significant and sustained demand growth across all markets, which has led to rent growth and (eventually) to new construction. Generally, demand for multifamily and industrial space continues to sustain new deliveries, but construction pipelines are sizable nearly everywhere, and could create some further localized distress when an economic slowdown occurs. This is consistent with Sentiment Survey respondents’ belief that multifamily and industrial, unlike most product types, are no closer to the peak than they were a year ago.

The second story, which can be applied to office and retail, features property types threatened by oversupply and/or structural obsolescence thanks to changing demand characteristics. Performance of these property types varies significantly across markets, though generally positive fundamentals (for office and retail) have resulted largely from very little construction (outside of rapidly growing tech and other “boom” markets). This will likely reverse when employment growth and consumer spending slow down.

Residential

- Multifamily demand exceeded supply in Q1 2019 for the first time since 2013; however, the pipeline of new supply remains elevated across most markets

- Nationwide, multifamily occupancy has increased in new, Class A product, albeit still below the long-term average

- Multifamily rents have exhibited stable growth since 2017

- Investor demand for multifamily product remains strong: transaction volume grew by 9.2% Y-o-Y, and multifamily transactions comprised 34.9% of investment activity in Q1 2019

- The overall sales volume of new single-family homes has remained essentially steady since Q2 2017; new home inventory (months of supply) remains noticeably above the long-term average, and the increase in inventory motivated builders to offer lower priced product, reducing the median price to drive absorption

- The market for existing single-family homes appears to still be relatively in balance, as inventory (months of supply) remains comfortably below the historical long-term average and median prices continue to trend upward.

Office

- National statistics paint a uniformly positive picture for office fundamentals: vacancy remains stable, rental rate growth has increased slightly, and absorption exceeds new deliveries

- Local statistics vary widely based on both local economic growth and market conditions

- Tech job growth has benefited markets like Atlanta, Austin, Boston, and the Bay Area, while job and household migration have benefited Sunbelt markets like Charlotte and Phoenix

- Construction activity, long dormant across the nation, remains moderately elevated nationwide, and excess supply is now evident in select markets, including NYC, Houston, and DC

- Class A absorption has remained consistent since 2017, while Class B has experienced a significant drop in net absorption recently

- Cap rate expansion/compression varied by market, with Atlanta, Orange County, and Philadelphia experiencing significant cap rate expansion

Retail

- This section focuses primarily on neighborhood/community center retail

- In general, a lack of new supply of neighborhood/community centers is sustaining performance in the face of broader challenges (such as changing shopper preferences, e-commerce, etc.)

- Occupancies have remained high at neighborhood/community centers, and rent growth has been low but generally stable across markets; outperforming markets benefit from strong job and population growth and limited supply

- Overall retail transaction volume spiked in Q2 2018 due to the Unibail Rodamco-Westfield transaction, before returning to previous volume levels

- Cap rates have generally been expanding for neighborhood/community centers and power centers, but malls experienced notable compression in Q1 (likely because only quality centers are transacting)

Industrial

- Construction activity has caught up with demand, with new supply outpacing absorption in Q1 2019

- Vacancy rates remain stable, however, and are below average in all major markets nationwide

- Industrial construction as a percentage of inventory has slowed, but remains only slightly below peak

- Rent growth has continued to increase nationwide (by over 5% YoY as of Q1 2019), and in supply-constrained markets has been exceptional

- Industrial transaction volume remains elevated at approximately $94B over the past year, and has increased by 19.8% YoY

- Cap rates compressed slightly over the past year, and remain at all-time lows

Hotel

- Q1 2019 occupancy, RevPAR, and ADR exceeded those of Q1 2018, and remain above peak levels

- Hotel transaction volume increased by 25.2% YoY, and comprised 6.4% of all transaction volume in Q1 2019

- Hotel cap rates continue to vary by market; nationwide, full-service cap rates remain relatively unchanged, while limited service cap rates dropped sharply, compressing 18 basis points since Q1 2018

Capital Markets Outlook

Returns continue to moderate as real estate capital market conditions continue to favor “sellers” of both property and debt investments, albeit at less feverish rates, with pricing for non-prime assets softening considerably in the past six months:

- Equity – Transaction volume remains robust; however, it has dipped from 2018 levels and has not kept up with fundraising efforts, leading to record levels of “dry powder.” Cap rate spreads to treasuries have dipped below their long-term average, likely pricing out some would-be real estate investors who are worried about where we are in the cycle. While cap rates have not moved much, asset pricing for non-prime assets relies more on current performance than on projected performance—an adjustment that has caught sellers by surprise.

- Debt – Net capital continues to flow into the real estate sector, led by commercial banks, life insurance companies, and the GSEs. Investment underwriting standards have remained relatively stable over the past year after years of loosening credit standards, leading to the availability of capital.

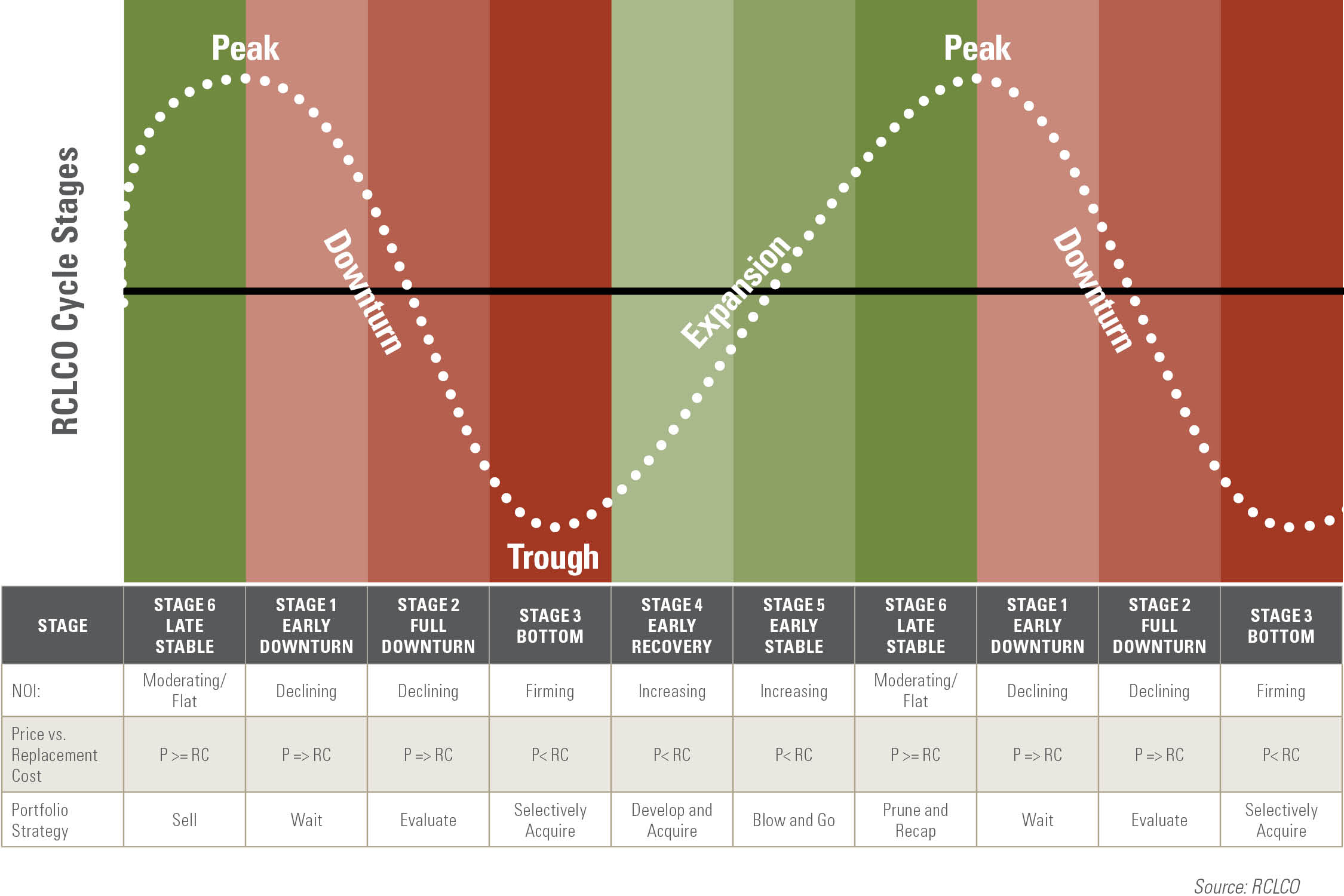

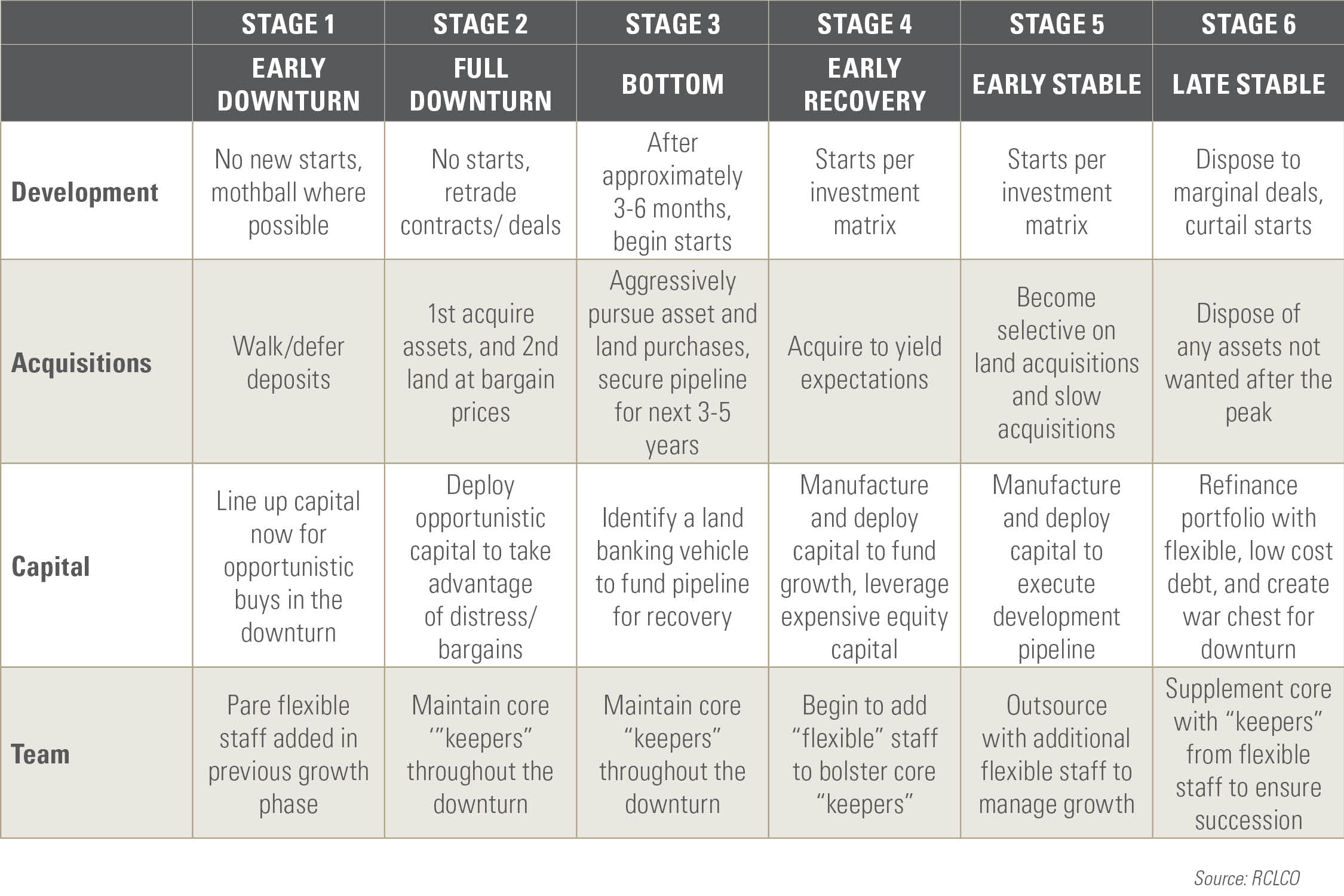

Real Estate Market Cycle Stages and Strategies

So, with most real estate segments bouncing around in the “late stable” phase of the cycle, and “early downturn” an increasing risk factor, it is important to talk about what companies in the real estate industry should be doing in response to changing economic and real estate market conditions.

For most real estate concerns, understanding the various cycle stages boils down to trends in income and the relationship between price and asset value and/or replacement cost. If you can divine the relationship between these few variables, you will have a better than average view of the real estate cycle. Trouble is, of course, clear patterns in these variables are not always easy to identify. Let’s focus on the current “late stable” stage and think ahead to the “early downturn” phase of the cycle.

Stage 6 —”Late Stable”

In the “late stable” portion of the cycle leading up to the peak, prices that market participants and investors seem to be willing to pay for assets (be they finished lots, raw land, stabilized income-producing assets, etc.) exceed asset values—not the inflated sugar-plumbs-dancing-in-your-head values, but the real, or, even, reasonable values of the asset.

If you are anything other than a very low-leverage long-term (as in generational) owner of real estate, this is the time to sell. This is the time to dispose of any marginal assets, or assets that are not wanted after the peak. This is also the time to refinance your portfolio with flexible, low-cost debt, and create a war chest for the downturn to take advantage of dislocations in the market.

One of the hardest decisions real estate executives have to make is to sell into what may feel like a continuing expansionary market. However, you must have courage into an upturn. The downside is that you may leave some money on the table between the time you sell and the actual peak. But by pulling the trigger sooner on assets you want to sell, you avoid not being able to sell them after the peak. At the peak, the market turns in an instant from a sellers’ market to a buyers’ market, and it may be very challenging to sell any asset you wanted to, at least at the price you had hoped for.

Stage 1 – “Early Downturn”

Following a cyclical peak, the economy and real estate markets enter the downturn. This is the stage when income, prices, and asset values are all falling. Credit is typically harder to come by on attractive terms, if at all, and most market participants try to go into sleeper mode. Developers curtail starts and mothball deals where possible. Acquirers try to defer, retread, and in many cases walk on deposits.

If you haven’t accumulated “dry powder” in the “late stable” stage, this is the time to begin to line up capital for opportunistic buys in the downturn. This is also the time when real estate companies pare down their overhead, ideally with flexible staff added in the latter part of the previous growth phase, and work hard to retain their “keepers.”

Companies that reach this stage without having deployed intermediary cycle strategies will be ill-prepared. These companies should have positioned themselves to take advantage of such adverse conditions. Instead, they become those who create opportunities for others. At this stage, the company’s strategic activities must be reevaluated. Investments and activities that made sense in a growing economy may not work in a downturn.

Early planning and ongoing monitoring will help provide real estate executives with the tools necessary to avoid getting in trouble. First, you need to have a comprehensive strategy for all portions of the real estate cycle. Then, you need to be nimble as you shift your activities from one strategic initiative to the next—from growth to hesitation to rationalization strategies. Last, you need to be able to anticipate so you can be among the first, not last, to realize what is going on and do something about it before it is too late. As you plan for and ultimately implement your cycle strategy, you must be prepared to act decisively, as history has shown how companies that hesitated too long often failed.

It is important to acknowledge that the current expansion is now the longest in history, and while the saying goes that expansions don’t die of old age, the risk that the U.S. economy and real estate markets will experience a period of slower growth (a.k.a., a recession) sometime in the future is increasing. Consistent with the feedback emanating from our recent Sentiment Survey (midyear 2019), RCLCO agrees that the probability of a real estate market downturn between now and 2022 is high, and while certainly not inevitable, contingency plans should anticipate it.

Article and research prepared by Charles Hewlett, Managing Director.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us